1. Crypto Networks Are Flourishing Amid The National Banking Crisis

Last week, while the US banking system seized up in response to bank runs, Bitcoin, Ethereum, and other crypto networks didn’t skip a beat. Crypto assets behaved like safe havens, as bitcoin appreciated ~20% over a 3-day period, between March 11th-14th.1

Despite mainstream rhetoric, equity and fixed income markets are beginning to recognize that crypto had nothing to do with the bankruptcies of Silicon Valley Bank (SVB) and Signature Bank. Instead, they began to implicate the U.S. Federal Reserve’s (Fed’s) ill-advised decision to push up interest rates 19-fold, a record-breaking rate, in less than a year.

In the face of the US and European banking crises, bitcoin’s price appreciation suggests that lax regulatory oversight had no impact on the decentralized, transparent, and auditable crypto asset ecosystem. Quite the opposite, bitcoin and other crypto assets are acting like safe havens. Last weekend, when many banks were closed and others were facing bank runs, Bitcoin didn’t skip a beat: it settled ~$33 billion, facilitated ~600k transactions, issued 2,037 new BTC at a steady and predictable ~1.8% inflation rate, attracted ~1 million new addresses, and generated $43 million for miners securing the network.2

Further, when Circle stablecoin USDC broke its peg to the dollar, SVB surfaced as the single point of failure in the US banking system, threatening on-ramps to the DeFi ecosystem. Despite the de-pegging of USDC and DAI, the Maker protocol remained over-collateralized and fully operational throughout the weekend,3 as the number of circulating DAI increased 25%, or $1 billion.4

Demand for more transparent, auditable, and decentralized financial services has soared because, in our view, crypto is a solution to the central points of failure, the opacity, and the regulatory lapses in the traditional financial system. Were it to become the scapegoat for policy mistakes in the traditional banking sector, crypto would move offshore, depriving the US of what we believe is one of the most important innovations in history.

Instead of blocking financial platforms that are decentralized, transparent, and auditable, with no central points of failure, regulators should focus on the centralized and opaque points of failure in the traditional banking system. Moreover, if the Fed continues to focus on lagging indicators like the Consumer Price Index (CPI) and employment and does not pivot in response to the deflationary forces telegraphed by the inverted yield curve and credit default swaps (CDSs), this crisis could devour more regional banks, centralizing—if not nationalizing—the US banking system. Crypto assets could be prime beneficiaries.

[1] Glassnode. March 14, 2023. Calculated from “Bitcoin: Price [USD].” https://studio.glassnode.com/metrics?a=BTC&category=&m=market.PriceUsdClose.

[2] Glassnode. March 11-12, 2023. Data are not entity-adjusted. Data from: “Bitcoin: Total Transfer Volume [USD]”; “Bitcoin: Number of Transactions”; “Bitcoin: Issuance [BTC]”; “Bitcoin: Inflation Rate”; “Bitcoin: Number of New Addresses”; “Bitcoin: Miner Revenue (Total) [USD].” https://studio.glassnode.com/.

[3] @MakerDAO Twitter. March 10, 2023. https://twitter.com/MakerDAO/status/1634410047592620034/photo/1.

[4] @fdowning Twitter. March 13, 2023. “Despite the USDC (and DAI) de-peg.” https://twitter.com/downingARK/status/1635356104334114816. Based on data from The Block, March 13, 2023. “Total Etheruem Stablecoin Supply.” https://www.theblock.co/data/decentralized-finance/stablecoins/total-stablecoin-supply-daily.

2. Coinbase and Circle Could Disrupt The Foreign Exchange Market

A few weeks ago during the Morgan Stanley Tech, Media & Telecom Conference, Coinbase CEO Brian Armstrong and CFO Alesia Haas discussed the company’s partnership with stablecoin issuer Circle, including potential use cases for Coinbase’s Ethereum Layer 2 network, Base, for zero-fee USDC transactions. Given Circle’s issuance of both USDC and Euro Coin, Base could disrupt the traditional USD-EUR cross-border transaction payment infrastructure that supported more than $62 billion in remittances—8% of $780 billion in global remittance volume—in 2021.1 Currently, Wise’s transaction fees to send $1,000 to and from Europe are 0.73% and 0.95%, respectively, incentivizing consumers to adopt stablecoins for cross-border transfers.2 If Base were to attract enterprises and financial institutions, Coinbase and Circle could disrupt the foreign exchange market, which, in 2022, facilitated ~$1.7 trillion in USD-EUR turnover per day—23% of global foreign exchange (FX) turnover.3

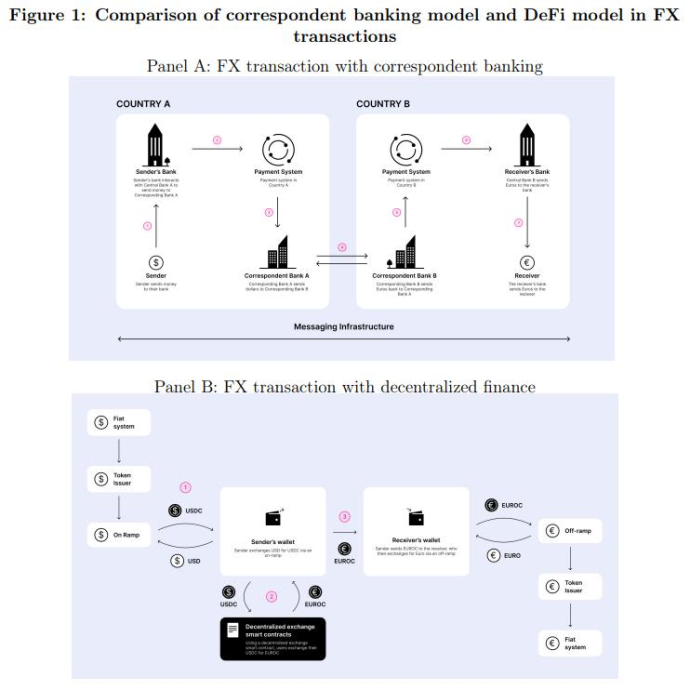

In our view, Base should be able to capitalize on inefficiencies in traditional cross-border payment by marketing zero-fee stablecoin swaps. For cross-border payments, stablecoins enjoy many advantages over traditional correspondent banking, including nearly instantaneous settlement, reduced settlement risks, transparency via public ledgers, and the democratized provision of liquidity. Traditional FX transactions require correspondent banks with accounts at various central banks debiting and crediting one other in the absence of standardization, as shown below.

Source: Adams, A. et al. 2023. “On-chain Foreign Exchange and Cross-border Payments.” Circle Internet Financial and Uniswap Labs. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4328948 (Page 4). For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency.

According to Circle and Uniswap, compared to the bank and money transmitter model, DeFi could reduce remittance costs ~80%. If Coinbase were to subsidize not only “traditional government-issued currency”(fiat) onramp/offramp fees but also Base Layer-2 fees for Circle-issued swaps, the only cost associated with stablecoin-based USD-EUR transactions would be the decentralized exchange fee ranging from 1 to 5 basis points per transaction.4 Circle also could subsidize USDC-euro coin swaps, potentially driving the total cost to zero. Powered by Application Programming Interfaces (APIs) like Coinbase’s Commerce API, businesses worldwide could adopt stablecoins, with Coinbase and Base potentially the prime beneficiaries.

[1] According to KNOMAD’s remittance data as of December 2022. We sum total remittance flows from and to the US and the 20 Eurozone countries that have adopted the euro as their official currency. We also include all flows within the 20 Eurozone countries.

[2] Wise is an online money transfer service.

[3] According to the Bank for International Settlements. According to McKinsey’s Global Payments Report, the commercial cross-border vertical generated nearly $180 billion in revenue in 2021.

[4] One basis point equals one hundredth of one percentage point.

3. Last Week Illustrated That Artificial Intelligence Is Ready For Prime Time

AI breakthroughs announced last week were nothing short of phenomenal and could revolutionize the way people interact with technology for years to come. Among them were the following:

OpenAI: GPT-4’s Astounding Performance Leap

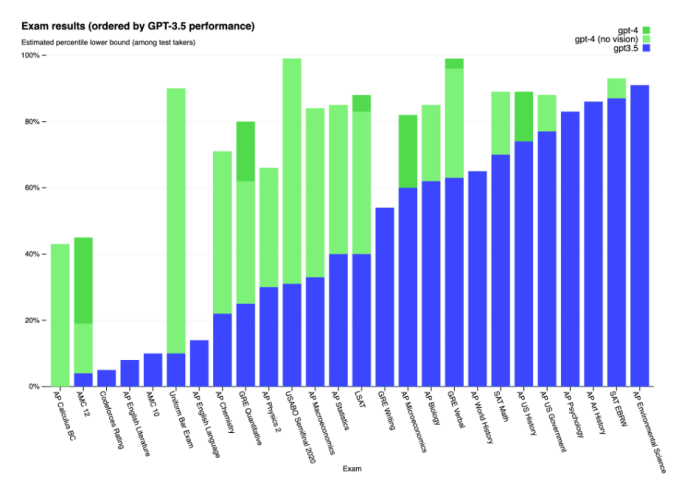

OpenAI released its much-anticipated GPT-4 model that achieved top percentile scores across a wide range of standardized tests spanning from law to calculus. GPT-4 highlighted the increasing power and versatility of AI models in tackling complex problems. On the Uniform Bar Exam, it scored in the 90th percentile, leaping from GPT-3.5’s 10th percentile, as shown below.

Image Source: OpenAI 2023. “GPT-4 Technical Report.” https://cdn.openai.com/papers/gpt-4.pdf (Page 6). For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency.

OpenAI has withheld many of the details associated with its GPT-4 model, perhaps because of significant competition brewing in the large language model space. We wonder if OpenAI’s competitors also will veer away from the open-source movement that has been so important in accelerating the development of AI models.

Productivity Apps Enabling AI Assistants

Also last week, Microsoft and Google disclosed ambitious plans for generative AI across their product lines, as Microsoft Office and Google Workspace added powerful, user-friendly features to everyday tools like Word, PowerPoint, Excel, Gmail, and Google Docs. They featured use cases leveraging AI to respond to emails, generate and copy-edit text, and create insightful charts from Excel spreadsheets based on simple natural language commands.

Midjourney’s Photorealistic And Human-Like Image Generation Model

In the realm of image generation, Midjourney released the fifth version of its image-generating diffusion model, offering higher quality, more photorealistic, and better humanlike images than earlier versions. The technology supports creativity previously unimaginable or prohibitively inexpensive for the entertainment, advertising, and design spaces.

Conclusion

Advances in artificial intelligence are accelerating much faster than even we anticipated. Last week’s developments could reshape human relations and increase knowledge worker productivity in profound ways during the next five to ten years.